The Platform Wars Are Coming for Finance

$4 billion in enterprise AI acquisitions. Finance operations hasn't been touched. Yet.

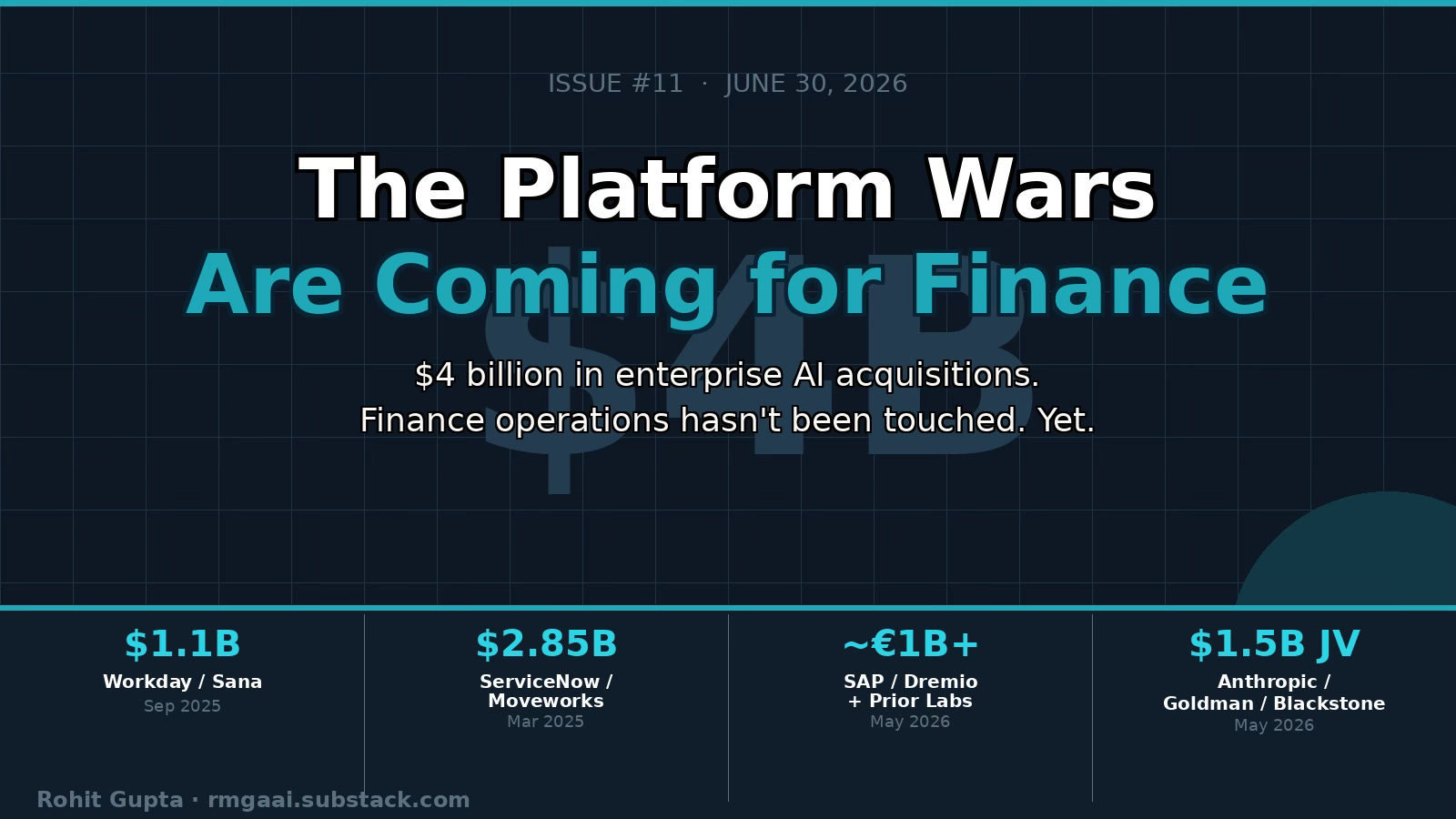

In the past 15 months, enterprise software companies have spent roughly $4 billion acquiring AI workflow specialists. Workday paid $1.1 billion for Sana. ServiceNow paid $2.85 billion for Moveworks. SAP ran a dual acquisition of Dremio and Prior Labs in what analysts are calling a billion-euro AI push. Anthropic partnered with Goldman Sachs and Blackstone to form a $1.5 billion enterprise AI services firm explicitly built to embed Claude into the operational workflows of hundreds of companies.

That is not a trend. That is a restructuring of the enterprise software map.

And if you run finance at a mid-to-large enterprise, you should pay close attention to what is happening, and to what has not happened yet.

What the pattern says

Each of these deals has a logic. Workday bought Sana because its HR and finance platform needed deeper AI agent capability for employee learning and workflow execution. ServiceNow bought Moveworks because enterprise employees needed a front-end AI layer that could navigate 100-plus enterprise systems without being told where to look. SAP acquired Dremio to unify SAP and non-SAP data into a single layer capable of powering agentic AI across the full ERP stack.

Every acquirer is solving the same problem: the platform has the data and the workflow infrastructure, but it lacks the specialized AI execution intelligence that turns that infrastructure into something employees actually use and trust.

That intelligence has to come from somewhere. Building it in-house takes years. The answer, consistently, is to acquire it.

This is the acquisition logic of the platform wars. The platforms become the infrastructure layer. The acquired specialists become the intelligence layer. The CFO or CIO who sits at the intersection pays the licensing fee but increasingly does not own either.

The gap nobody is talking about

Here is what strikes me about the acquisition map so far: every deal targets HR, employee productivity, IT workflow, and data infrastructure. The enterprise function that has been conspicuously absent from the acquisition conversation is finance operations.

Not fintech. Not payments. Not trading infrastructure. Finance operations: accounts payable, accounts receivable, cash cycle management, multi-entity financial orchestration. The day-to-day execution layer that sits between your ERP and your cash position.

Consider the scale of what’s at stake. AP automation alone is valued at $6.94 billion in 2026, projected to reach $12.46 billion by 2031. Add AR automation — billing, collections, cash application, dispute management — and the combined Finance Operations automation market sits at nearly $11 billion today, growing toward $19 billion by 2031. And yet, according to recent industry data, 66% of AP teams are still manually keying invoices into ERP or accounting software. Seventy-three percent have not fully automated core AP workflows. That’s not a gap. That’s an unsolved category sitting in plain sight, inside virtually every enterprise already using Workday or SAP.

The platform vendors know this. They just have not moved here yet.

Why finance workflow AI is different

Building AI for finance workflow is not the same as building AI for HR workflow or IT service desks. The complexity is different in kind, not just in degree.

Enterprise finance is operationally critical and compliance-intensive by definition. An exception in HR workflow is a missed alert. An exception in AP workflow is a payment timing error, a cash position gap, a DPO calculation running on incomplete data. The margin for silent failure is essentially zero.

More importantly, finance workflow AI requires proprietary execution intelligence. To actually process invoices at enterprise scale across multiple geographies, currencies, and legal entities, a system needs to understand vendor behavior, invoice format patterns, exception taxonomies, and cash cycle outcomes at transaction level. That intelligence does not come from a foundation model. It does not come from a data lakehouse. It comes from millions of actual finance transactions, processed in production, across real enterprise environments.

This is the moat that no acquisition target can manufacture quickly. It has to be built over time, in production, against real complexity. It is the reason the platforms have not moved here yet.

What force amplifier actually means

The term I use internally when I talk about Auditoria’s role is “force amplifier.” I want to explain what that means precisely, because it is easy to mistake it for marketing language.

Workday is in over 10,000 organizations globally. SAP runs the financial backbone of most of the Fortune 500. These platforms are not going away. They are not being replaced. What they need is the finance execution intelligence layer that makes them deliver on the promise of AI-powered finance operations.

Auditoria is that layer. We process invoices across global enterprise environments with no templates, adapting to each supplier on the first read. We give finance teams real-time cash visibility across entity stacks that are often dozens of entities deep. We handle the AP execution that happens between when a transaction enters the ERP and when it clears. That range is where the cash cycle is actually won or lost, and it is the range that Workday, SAP, and ServiceNow do not currently own.

When I say force amplifier, I mean this: the platform makes the enterprise run. Auditoria makes the finance function within that enterprise run at the speed and intelligence level that the platform alone cannot reach. The two are complementary, not competitive. That’s not a positioning statement. That’s an architectural fact.

There is a third dimension worth naming here. AP execution and AR execution are layers one and two. Layer three is cash cycle intelligence: the autonomous synthesis of what is happening across AP and AR operations in real time, correlated with external signals, to produce a continuous, actionable view of your cash position, working capital exposure, and DPO and DSO trajectory. Not a report. Not a dashboard. An intelligence system that surfaces what matters before anyone has to ask.

This is the layer that no platform acquisition has yet reached. The ERP vendors have reporting modules. The frontier model providers have general-purpose reasoning. Neither is the same as autonomous finance intelligence built specifically for the cash cycle. The force amplifier is not just execution. It is execution plus intelligence plus cash cycle ownership. That full stack is what none of the players currently racing for the Finance Operations gap have assembled.

The window

Here is the part of this that I think about most.

The acquisition pattern will reach finance. The logic is too clear, the market too large, and the gap too obvious for platform vendors to ignore indefinitely. The question is not whether; it is when, and who is left standing independently when it happens.

The companies that build genuine execution intelligence in this window, with real transaction data, real enterprise deployments, real cash cycle outcomes, are the ones that own the category when the consolidation arrives. The ones that are still assembling the platform or licensing generic AI capability into a finance wrapper are not.

We are in the window right now. The AP automation market is growing at over 12% annually. Seventy-three percent of enterprise finance teams have not fully automated their core workflows. Every one of those is a deployment opportunity that builds proprietary execution intelligence. Every quarter we are in production at another global enterprise is a quarter that advantage compounds.

The platform wars are coming for finance. The force amplifier that makes them land has to be in place before the war arrives.

What I would want every CFO to consider

Two questions I would bring to your next operating review:

When your AP system touches an invoice it has never seen before, what happens? Does it adapt, or does it escalate? The answer tells you whether you are running an execution system or a routing system.

And: if one of the platform vendors you are already paying absorbed your AP workflow AI tomorrow, would you get the same outcome? Or would you get a general-purpose capability wrapped in a familiar interface?

The answers locate you on the map.

If you want to work through what AI-augmented execution actually looks like against your specific invoice set, your entity count, and your current exception rate, reply here or book 20 minutes. The conversation is worth having before the consolidation decides it for you.

Rohit Gupta is CEO and Co-Founder of Auditoria.AI. The Auditoria platform operates the cash cycle, processes invoices, automates collections and deliver financial insights across global enterprise environments using agentic AI, no templates required.

Sources: Workday newsroom, September 2025; ServiceNow newsroom, March 2025; SAP newsroom, May 2026; CNBC / Anthropic, May 2026; Mordor Intelligence, AP Automation Market, 2026; Mordor Intelligence, AR Automation Market, 2026; ReceiptsAI AP Automation Statistics, June 2026.

An interesting perspective on how finance operations fit into the broader enterprise AI landscape. As organizations evaluate these capabilities, the ability to improve execution across AP, AR, and the cash cycle while integrating with existing processes will be a key differentiator.